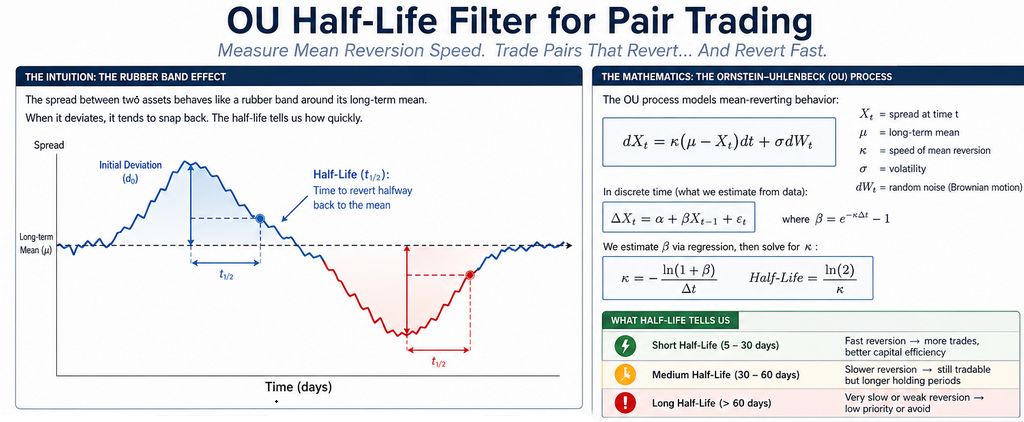

One of the biggest hidden risks in pair trading isn’t finding a cointegrated relationship. It’s trading a pair that reverts too slowly to be profitable before costs, time decay, or market drift eat your edge.

That’s exactly why we’re adding the OU Half-Life Filter to PairTrade Finder® Ultimate Alpha 3. It’s a simple, powerful new layer that tells you how fast a spread will snap back — so you only trade the pairs that can actually make money in real-market conditions.

Why Many Pairs Fail in Live Trading (Even If They Pass Backtests)

Why Many Pairs Fail in Live Trading (Even If They Pass Backtests)

You run the scanner.

… Read More →