Faster Reversion = Better Profits in PairTrade Finder® UA3

One of the biggest hidden risks in pair trading isn’t finding a cointegrated relationship. It’s trading a pair that reverts too slowly to be profitable before costs, time decay, or market drift eat your edge.

That’s exactly why we’re adding the OU Half-Life Filter to PairTrade Finder® Ultimate Alpha 3. It’s a simple, powerful new layer that tells you how fast a spread will snap back — so you only trade the pairs that can actually make money in real-market conditions.

Why Many Pairs Fail in Live Trading (Even If They Pass Backtests)

You run the scanner.

You see strong correlation.

ADF cointegration looks good.

Backtest looks profitable with good reward/risk, win rate.

Then live trading happens and… nothing. The spread just wanders.

The OU Half-Life Filter seeks to fix this situation by removing statistically valid but economically useless pairs before they reach your Watchlist.

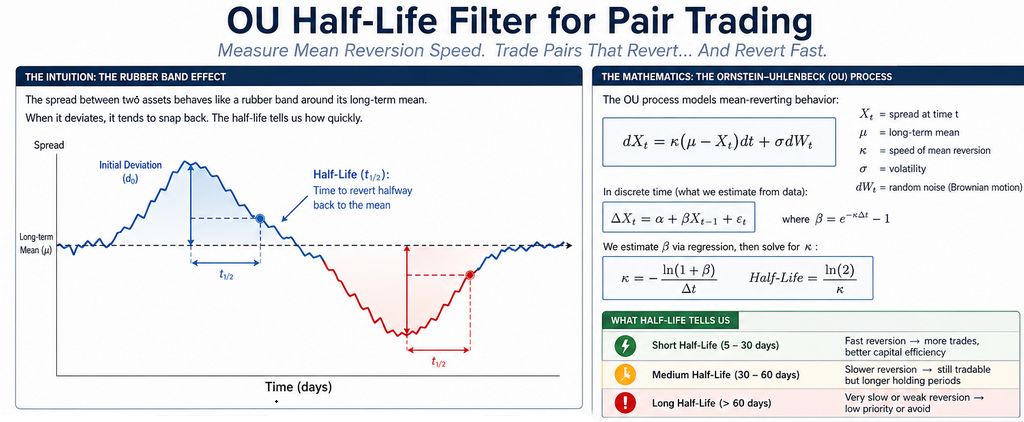

Academic Validation: Why This Works

The foundations are well established in peer-reviewed research. Mean-reversion speed — captured by the OU half-life — is central to both trade selection and execution. It determines not only whether a spread is tradable, but also optimal holding time and where entry/exit thresholds should sit.

Gatev, Goetzmann & Rouwenhorst (2006) demonstrated persistent mean-reversion profits in U.S. equities using distance rules. Avellaneda & Lee (2010) took the next step, modeling spreads as Ornstein-Uhlenbeck processes and showing that “incorporating mean-reversion dynamics significantly improves Sharpe ratios and robustness.”

Subsequent work by Leung & Li (2015) and Bertram (2010) proved that optimal entry and exit thresholds are functions of mean-reversion speed — not fixed constants. In short, half-life is the missing filter that turns good-looking pairs into reliably profitable ones.

How We’re Adding the OU Half-Life Filter to PairTrade Finder®

(Clean, simple, zero disruption to your current workflow)

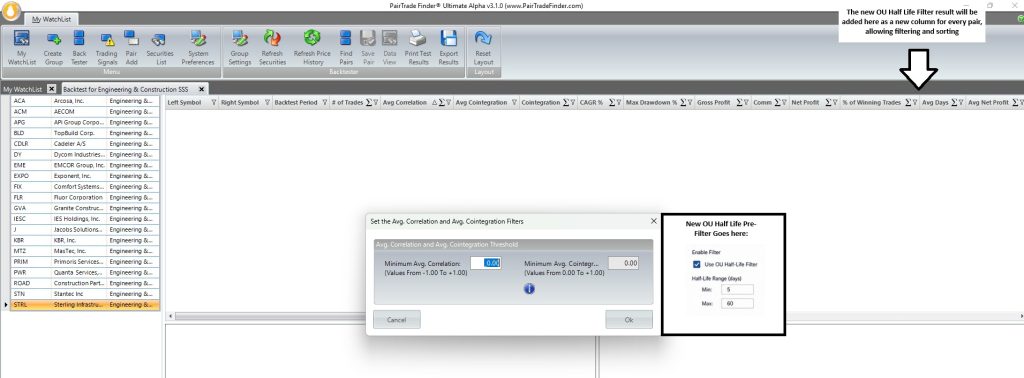

- Optional Pre-Filter

To be added alongside ADF p-value, correlation, sector, and business-fit checks. The scanner runs the half-life calculation on the spread series (log-price-ratio residuals) in the background. Only pairs within your chosen min/max range move forward into the backtester. - New Column in Backtester Results

“OU Half-Life (days)” will appear in the results grid. Sort, filter, or export exactly as you do today.

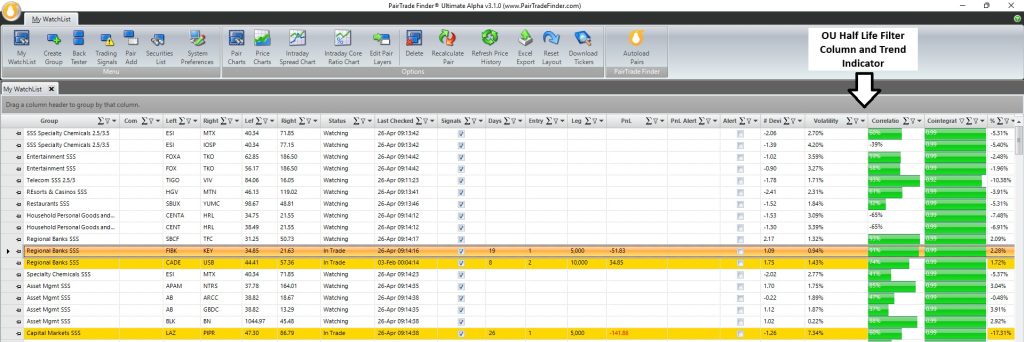

- Watchlist / Radar Upgrade (The Real Game-Changer)

Every pair in My Watchlist will soon show a live, intraday-updated half-life (recalculated on the most recent 90–252 bars). Plus a small trend indicator: - 🟢⬇️ Arrow down = half-life shortening → reversion accelerating (even better)

- 🔴⬆️ Arrow up = half-life lengthening → reversion slowing (warning)

Where the OU Half Life Filter Really Adds Value (vs. Average Days In Trade)

PTF UA3´s backtester already shows “Average Days in Trade” — a useful post-trade outcome metric under a set of specific trading parameters e.g. 2.7 SD entry / 1.0 SD exit rules. The OU Half-Life is different and complementary:

- Pre-selection efficiency

Screen 10,000+ pairs in seconds and discard anything >45 days before backtesting. Average Days can’t do this — it only appears after the full backtest runs

- Robustness & orthogonality

Model-driven and threshold-agnostic. Stays valid even if you change SD levels or add filters. Average Days is tied to your exact rules

- Live monitoring & dynamic management

Rolling 90- or 252-day half-life updates in real time. Lengthening half-life is an early warning to reduce size or drop the pair — long before Average Days updates

- Exit timing & risk management

Expected remaining reversion time is directly tied to current deviation + half-life. Use it for dynamic rules (e.g., “if half-life >35 days, cut size 30%” or “exit if trade duration exceeds 2× half-life”)

- Research-backed performance lift

Short-half-life pairs consistently deliver higher win rates, better profit factors, and smoother equity curves out-of-sample.

From Filters to Intelligence: The PairTrade Finder® Ultimate Alpha 3 Super Stack

With the addition of the OU Half-Life Filter, and the other two indicators outlined in our previous two blog posts, PairTrade Finder® will soon operate as a four-layer pair trading signal intelligence system:

- Statistical Validation (current PTF): Cointegration + correlation + sector + liquidity + business fit

- News Shock Score: Avoids signals driven by fundamental corporate events

- Relative Edge Score: Dynamic, regime-sensitive technical confirmation on each leg

- OU Half-Life Filtering & Dynamic Monitoring: Ensures fast reversion and lets you optimize entry/exit on a pair-by-pair basis as markets evolve

Why This Super Stack Changes Everything

Most traders use 1–2 layers. You will shortly have 4. This transforms your process from stating “This pair trade looks good” to:

“This pair trading signal is structurally valid, isn’t driven by a corporate action, is technically supported, and is likely to revert quickly.”

The Targeted Outcome

- Higher-quality trades

- Faster capital turnover

- Reduced drawdowns

- More consistent performance

Start Your Free Trial

If you’re still relying on correlation and cointegration alone, you’re leaving edge on the table.

Start your free trial of PairTrade Finder® UA3 today!

Happy trading,

The PairTrade Finder® Team

Research Appendix:

Gatev, E., Goetzmann, W.N. and Rouwenhorst, K.G. (2006)

Pairs Trading: Performance of a Relative-Value Arbitrage Rule. Review of Financial Studies, 19(3), pp. 797–827.

→ Found persistent mean-reversion profits in U.S. equities.

Avellaneda, M. and Lee, J.-H. (2010)

Statistical Arbitrage in the U.S. Equities Market. Quantitative Finance, 10(7), pp. 761–782.

→ Demonstrated improved performance using OU-based modelling of spreads.

Leung, T. and Li, X. (2015)

Optimal Mean Reversion Trading: Mathematical Analysis and Practical Applications. World Scientific.

→ Shows optimal entry/exit thresholds depend on mean-reversion dynamics.

Bertram, W.K. (2010)

Analytic Solutions for Optimal Statistical Arbitrage Trading. Physica A, 389(11), pp. 2234–2243.

→ Derives optimal trading rules based on OU processes.

Zeng, Z. and Lee, C.-G. (2014)

Pairs Trading: Optimal Thresholds and Profitability. Applied Economics Letters, 21(14), pp. 994–997.

→ Confirms threshold optimisation improves returns.